Hey there, Cam Dunlap here.

I get asked all the time how to find motivated sellers.

But lately I’ve been getting a more specific version of that question, and it’s the right one to be asking: how do I find pre-foreclosure leads?

There’s a reason that question is coming up more. Foreclosure activity is climbing.

It’s nowhere near 2009 levels — not even close — but it’s meaningfully up. People who grabbed forbearances during COVID and have been treading water for years are finally running out of runway. Add in what’s happening with unemployment and the overall economic noise right now, and you’ve got a growing pool of homeowners who need help.

That’s not a bad thing to say. I’m not celebrating anybody’s hardship. But I’ve been doing this for over thirty years, and I know that the people who are willing to step into that gap, treat those sellers with respect, and actually solve their problem are the ones who do the most deals.

Pre-foreclosures are one of the highest-motivation categories in this business. Here’s how to find them.

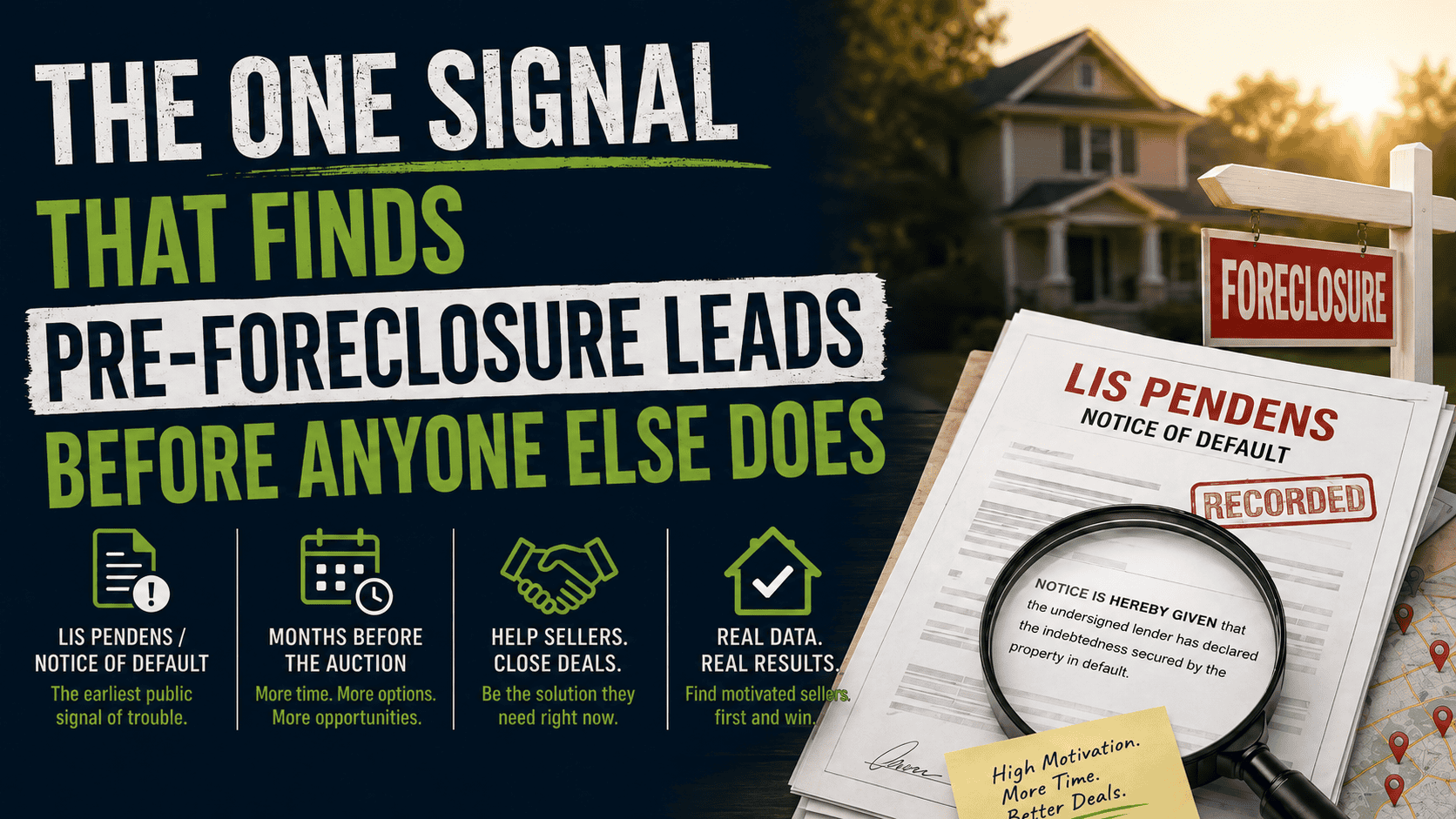

The Single Best Signal: Lis Pendens and Notice of Default

There is one signal that cuts straight to the highest-motivation pre-foreclosure leads, and it’s called Notice of Default — or in some markets, Lis Pendens.

Same thing, different name depending on where you’re working. Here in Florida it’s Lis Pendens. In upstate New York it’s Notice of Default, or NOD. The underlying event is identical: the lender has recorded notice on the public record that the borrower has stopped making their mortgage payments.

This is a legally required filing. The bank doesn’t do it because they want to — they do it because the law requires it. And once it’s recorded, it’s public information. Which means it’s searchable, and you can get in front of those sellers.

What the Filing Actually Means

Most lenders wait until a borrower has missed three consecutive payments before filing. That’s roughly ninety days. So by the time that notice hits the public record, you’re looking at a seller who has been sitting on a problem for three months already.

That does not mean they’re ready to sell. Some are. Some are still in denial. Some are in the anger stage, some are bargaining with the bank. But they are all, by definition, under pressure in a way that most sellers are not.

And here’s the part that matters for you: they still have time. The foreclosure sale hasn’t happened. There’s still a window for them to do something, and what they need is someone who can actually move fast and help them out of the situation with their dignity intact. That person can be you.

Why Lis Pendens Is Different From Foreclosure Auction Lists

A lot of investors only start paying attention once a property has a scheduled auction date. By that point, you’ve got days or weeks to act, the owner is buried in stress, lenders are involved in every conversation, and the window to do a clean deal is extremely narrow.

When you work the lis pendens list, you’re getting to the seller months before the auction. There’s time to have a real conversation. There’s time to structure something that works. There’s time to stop the foreclosure process entirely if you or the seller can get a contract to the lender and demonstrate that the deal is going to close.

Banks don’t want these houses. They really don’t. If you can show up with a signed contract and a legitimate close date, there’s a real chance the bank will work with you to postpone the sale if it’s close. It’s not guaranteed, but it happens, and it generally doesn’t happen for investors who show up the week of the auction.

What About Bankruptcies and Liens?

I get this question a lot. The short answer is that liens can absolutely accompany a pre-foreclosure — a house going into foreclosure might have mechanic’s liens, HOA liens, and other claims on it all at once. That’s part of what you need to evaluate when you’re running your numbers.

Bankruptcy is a different animal. It sometimes follows a notice of default as a stall tactic — the seller or their attorney files bankruptcy to trigger an automatic stay and buy more time. It can freeze the foreclosure process for months. If you’re in contact with the seller early, before they’ve taken that route, you may be able to solve their problem before they feel the need to go that direction.

Go Find These Leads in the Real Estate Data Feed

The Lis Pendens and Notice of Default filter is available right inside the Real Estate Data Feed. Log in, pull up the motivated seller dataset, and it’s one of the filters you can apply. You can layer it with other criteria — property type, geography, equity position — to get a list that’s as targeted as you want.

The data is updated regularly, which matters here. This isn’t the kind of list where you run it once and mail it six times over a year. Pre-foreclosure windows move to fast for that. You want fresh data and velocity.

If you haven’t tried the Real Estate Data Feed yet, there’s a 100% risk-free test drive available right now. Get in there, filter for lis pendens in your market, and see what’s sitting in front of you right now.

The Investor Who Gets There First Wins

When a lis pendens hits the public record, you’re not the only one who can see it. Other investors can see it too. The ones who set up a system to pull fresh filings and reach out fast are the ones who get the conversation before the seller has already been through three different pitches from three different people who all left them feeling worse than before.

Be the one who shows up early and treats them like a person, not a data point. Ask good questions. Find out what they actually need. Make the math work for both of you.

That’s how you turn a motivated seller list into a deal.

Regards,

Cam Dunlap