If you are like most investors, writing offers can be a major stumbling block.

Contracts look intimidating, knowing the right price to offer seems overwhelming, and the anticipation of what will happen next can be frightening.

After a couple decades of doing deals, I know what you are going through.

I have streamlined my offer making process, and I would like to share it with you…

My 7 Step Streamlined Process For Making Offers

(We’re talking about houses owned by private sellers. Bank sellers are very different!)

- Make the Contract Assignable

If you are using a Realtor contract,there is probably language that prevents you from assigning the contract (or a checkbox that asks you if the contract is assignable). But, in order for you to make quick cash without using your own money, you have to be able to assign your contract, so that needs to change. You can change the language in the Realtor contract, hire an attorney to create a customized contract for you, or you can use the same contract I and many of my students have been using for years inside my “Purchase & Sale Agreement Line By Line” course. An old school method is to put the words “and or assigns” where the buyer is named. So it would read “ABC Real Estate Solutions, Inc. and-or assigns”. This works but can raise questions in the eyes of the seller, which is, as mentioned above, not a good idea.

- Make a Cash Offer

The buyer you wholesale the property to should be paying cash for the house, so you can ethically make a cash offer. By doing this, you make the seller comfortable because they know that you are not going to a conventional lender who would not approve this house for a conventional loan because of its condition.

- Close on the Date of Their Choice

One big mistake that most investors make is saying, “We’ll close fast” or “close in 10 days” in their marketing for motivated sellers.

Sometimes sellers want to close as fast as possible, while other sellers need to make some arrangements and therefore DON’T want to close fast. By being flexible on the closing date, you are accommodating sellers in any situation.

One time I was working with a motivated seller who wanted to close in 90 days. She needed time to find a trailer for her sons. I drove through a trailer park and called theFSBO sign on a property that looked like a good fit. The seller happened to be across the street and he showed it to me immediately. He wanted $5,000 for it… and she wanted to pay $5,000. So I offered him $3,000 and got it. I wholesaled it to my motivated seller and made a couple extra thousand dollars. Not only that, she was ready to close right away, so I didn’t have to wait 90 days to get paid on the first deal.

When you use the phrasing “close on the date of your choice” in your marketing you’ll find that more doors of opportunity open up for you.

- Earnest Money

I rarely use more than $10 for earnest money when working with private sellers. Sometimes I go up to $100. Sellers really don’t care! Most would never even mention it, if I didn’t bring it up. And the reason I bring it up is because money serves as a definite means of consideration. In order for a contract to be enforceable, “consideration” is required and nobody can argue that money is not consideration. I use the word “legitimate” when I describe this to a seller.

If you are working with a bank, the earnest money is usually at least $500 or 1% of the purchase price (whichever is greater) and you don’t have as much flexibility with institutional sellers. While it is part of the negotiation, they have had TOO many deals fall apart and they want you to have “skin in the game”.

- Proof of Funds

With banks, this is a requirement. They want to know that you have the means to close. They want you to prove that you have cash available. With private sellers, this is practically a non-issue. I have had a few ask me to prove my ability to fund, but it is very rare.

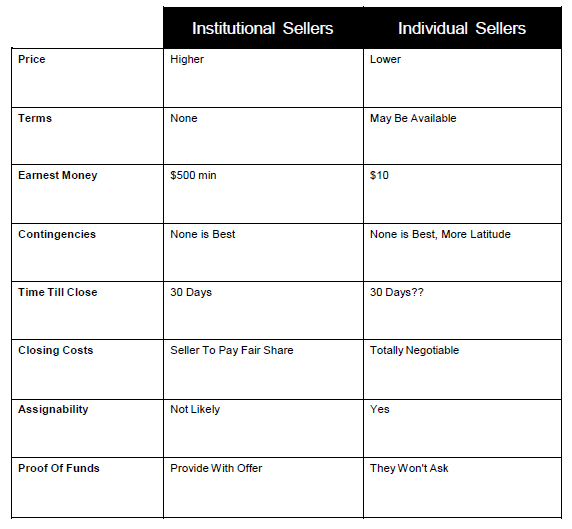

Here is a matrix I put together to help you understand the differences between private sellers and bank sellers:

If you don’t have the funds available in your own personal bank account there are ways to still get valid proof of funds letters to do your deals. In fact, that’s one of the many benefits inside my “4 Pillars of Real Estate” Program.

- Presenting Your Offer

Faxing or emailing your offer to a seller is acceptable. If you live in another state, it is usually the only way these deals get done. But, if you live locally, I would highly recommend doing it in person. If they can shake your hand, look you in the eye, and they like you… there is a higher probability that they will sell to you, at your price.

If you are a “virtual” person, they may have questions and doubts that never get reconciled because you can’t see the look on their face when they read the contract. You may not like the idea of presenting a low offer in person, but I will tell you, they aren’t getting any other offers AND they are well aware of the poor condition and the high price tag to fix the house up. In my experience, the seller thinks the house will cost twice as much to fix up as what my buyer can get it done for. So while it may feel to you, like you made a really low offer on the house, they may think it is really fair.

- Submit Your Contract to Your Closing Agent

Once you get a signed contract with your seller, send it over to your closing agent or Real Estate attorney. I prefer to use attorneys on all of my transactions (even for my deals in non-attorney states). Attorneys add a layer of protection that I am comfortable with and they handle all of the paperwork (so I don’t have to). Once you turn your contract in to your attorney or closing agent, you are ready to find your buyer and get paid!.

**If you DO NOT already have a list of cash buyers for your deals you will want to try out the Cash Buyer Data Feed. It’ll give you instant access to all of the cash buyers in your area (and around the country) that are actively buying properties for cash. We are currently running a trial offer at a ridiculously low price on the Cash Buyer Data Feed.

When putting an offer on a house your job is to make it easy for the seller to say “yes”.

The value you bring to the table is a quick, hassle-free offer to purchase that has a high probability of closing.

The right seller – a motivated seller will see real value in your solution.

Pro Tip: Truly motivated sellers are willing to trade equity for peace of mind.

For example, I once received a call from a probate attorney who said they needed a quick real estate offer. I would have paid $150,000 for this house but when I asked him what they were looking for, he said $85,000. I was super excited…until I heard that the neighbor was making an offer on the house too. I didn’t want to get into a bidding war so I asked the attorney for more info and found out that the other offer had contingencies. Not only did my offer on the property not have any contingencies, I went one step further… I made my earnest money deposit in the amount of $85,000. This guaranteed them the cash they wanted for the house… and whose offer do you think they accepted? Yep… mine!

There is only one contingency that I use (and I would always recommend for every buyer no matter what kind of deal)… clear title.

I ALWAYS want (no, NEED) to know if there are any other liens or encumbrances on the property. If I put down $85,000 in earnest money and find out at closing that there are $200,000 worth of liens on the property that the seller did not tell me about… I am in big trouble!

I have never had a seller complain about checking title… it is common practice… and if they had a problem with it… that would be a big red flag and I would quickly back away.

Follow these 7 steps to making an offer on a house and you’ll find that you get more offers accepted, which of course means more profits in your pocket!

If you would like a complete guide on flipping a house with no money, credit, or experience (in 30 days or less), check out my blog post on Flipping Houses With No Money.

Thanks for reading!

Best Regards,

Cameron Dunlap